11/25/2024

Gold and silver hit hard by revived risk-on sentiment

OUTSIDE MARKET DEVELOPMENTS: Markets have been cheered by President-elect Trump's broadly appealing choice of Scott Bessent for Treasury Secretary. This has boosted risk appetite offsetting some of the risk-off flows associated with hot geopolitical tensions between Russia and the West.

Bessent is known to be a fiscal hawk who will hopefully be keen to address America's surging debt burden, which is now more than $36 trillion. To accomplish that and keep the economy on an even keel, Bessent may seek to temper Trump's campaign promises for aggressive tax cuts and tariffs.

Stocks and Treasuries are higher. Lower yields have pulled the dollar index off last week's 13-month high.

Geopolitical risks remain elevated. Russia and Ukraine continue to trade missile and drone attacks. NATO is slated to hold an emergency meeting with Ukraine on Tuesday over Russia's use last week of an experimental hypersonic weapon.

Meanwhile, on Sunday Hezbollah launched its largest rocket barrage in months against Israel. Despite this attack, Israeli PM Netanyahu has reportedly "agreed in principle" to a ceasefire deal with Hezbollah which is contributing to revived risk-on sentiment.

U.S. Chicago Fed National Activity Index fell 0.13 points to -0.40 in October, below expectations of -0.20, versus a negative revised -0.27 in September. All four categories used to construct the index made negative contributions. This index remains quite choppy.

U.S. Dallas Fed Manufacturing Index edged higher to a 31-month high of -2.7 in November, below expectations of -2.4, versus -3.0 in October. Though still in negative territory, the index has been tracking higher since August.

GOLD

OVERNIGHT CHANGE THROUGH 6:00 AM CST: -$26.83 (-0.99%)

5-Day Change: +$20.32 (+0.78%)

YTD Range: $1,986.16 - $2,789.68

52-Week Range: $1,812.39 - $2,789.68

Weighted Alpha: +26.60

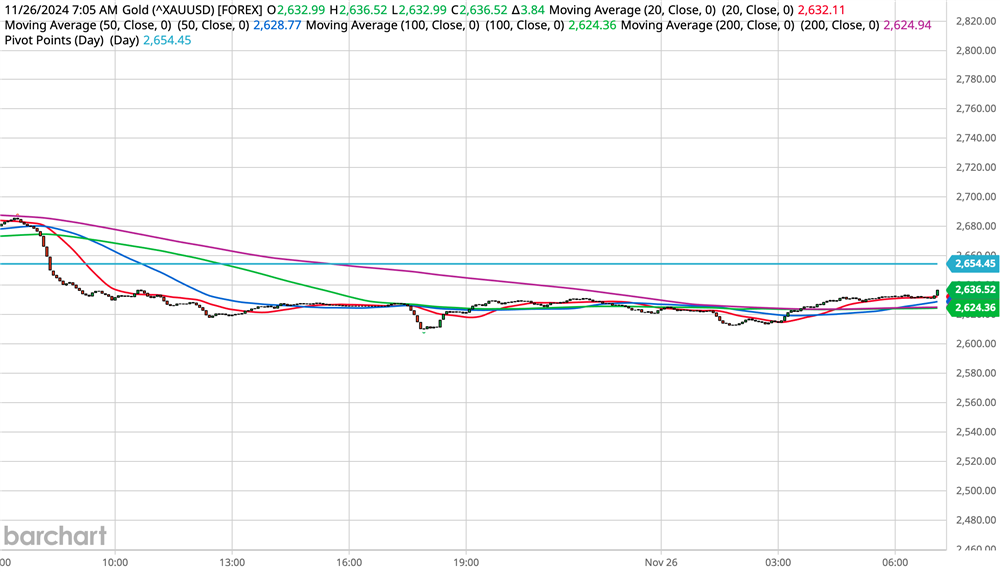

Gold has come under significant selling pressure amid revived risk appetite, notching the biggest one-day drop since 07-Jun when we saw surprisingly strong May jobs data. The yellow metal has retraced about half of last week's solid gains.

President-elect Trump's nomination for Treasury Secretary and optimism about a possible ceasefire between Israel and Hezbollah have shifted market focus to riskier assets and away from havens like gold.

However, the conflict between Israel and Hamas continues and tensions between Russia and the West remain extremely high. Any escalation in either theater could quickly swing market sentiment back toward risk-off.

I still anticipate a 25 bps rate cut in December, but recent FedSpeak has taken on a more cautious tone heading into 2025, which also poses a bit of a headwind for gold. Prospects for a December hold continue to hover around 40% but became close to a 50-50 proposition on Friday.

Global ETFs saw a modest net inflow of 3.4 tonnes last week on heightened geopolitical risks, ending the string of weekly outflows at two. North American buying eclipsed outflows from Europe and Asia.

Futures traders were apparently less inclined to buy into last week's rally. The latest CFTC COT report showed net speculative long positions fell 2.1k to 234.4k contracts in the week ended 22-Nov from 236.5k contracts in the previous week. It was the fourth consecutive weekly decline.

CFTC Gold speculative net positions

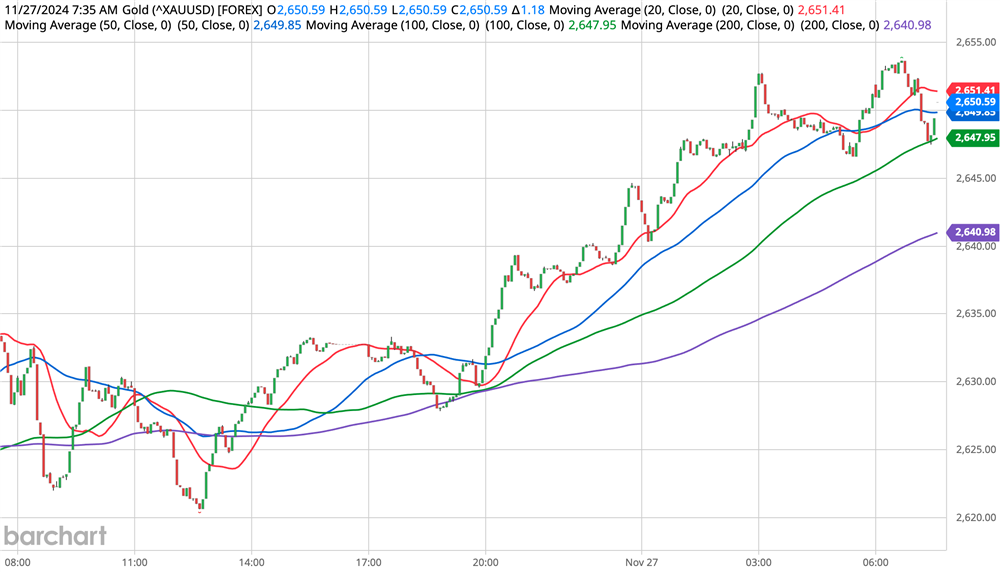

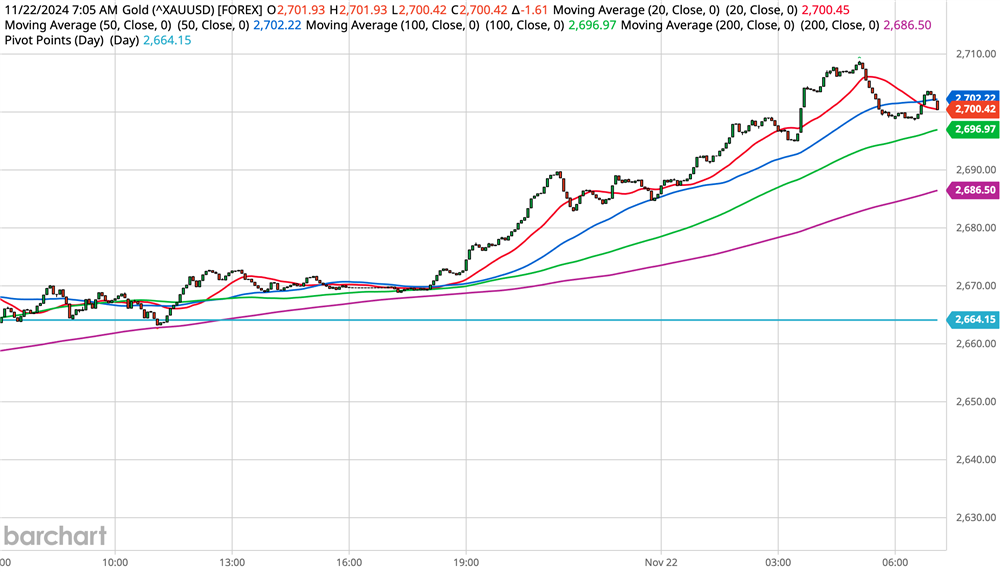

Last week's gains back above $2,700 went a long way toward suggesting the corrective low is in place at $2,541.42. From there I was expecting choppy consolidative trading to prevail into year end. Today's price action reinforces that expectation with competing risk-on/risk-off forces competing for the attention of investors.

I suggest that such a consolidation phase would bode well for an eventual continuation of the long-term uptrend. A rebound above $2,668.84/$2,669.91 would ease pressure on the downside and suggest potential for further probes above $2,700.

With gold back below the 20- and 50-day moving averages, the short-term bias is back to the downside. Supports to watch are at $2,621.25 (20-Nov low) and $2,610.94/$2,609.54. The latter is marked by the low from 19-Nov and 61.8% of the rally off the $2,541.43 cycle low.

SILVER

OVERNIGHT CHANGE THROUGH 6:00 AM CST: -$0.508 (-1.62%)

5-Day Change: -$0.986 (-3.16%)

YTD Range: $21.945 - $34.853

52-Week Range: $20.704 - $34.853

Weighted Alpha: +27.84

Silver plunged more than 3% in sympathy with gold. The much smaller, more thinly traded silver market has a higher beta that lends itself to amplified moves, particularly on the downside.

Despite the recent swings, the white metal remains confined to the range established in the week ended 15-Nov. However, today's breach of last week's low at $30.260 and the move back below the 100-day moving average suggests the $29.736 cycle low from 14-Nov remains vulnerable to a challenge.

Unlike gold, last week's gains in silver failed to signal that the corrective low was likely in place. I was watching the 20- and 50-day moving averages and the $32.294 Fibonacci level for that confirmation.

The CFTC COT report for last week showed net speculative long positions declined by 1.3k to 46.3k contracts, versus 47.6k in the previous week. While the decline was slight, it was the fourth consecutive weekly decline in net spec long positioning.

CFTC Silver speculative net positions

The 20- and 50-day MAs are at $31.551 and $31.787 respectively and are protected by solid chart resistance at $31.417/465. A rebound through this zone is needed to reinvigorate the bull camp.

I still think we could get a range form as long as gold holds its low. However, a fresh cycle low in silver below $29.736 would shift focus to the rising 200-day moving average at $28.970.

Peter A. Grant

Vice President, Senior Metals Strategist

Zaner Metals LLC

Tornado Precious Metals Solutions by Zaner

312-549-9986 Direct/Text

[email protected]

www.ZanerPreciousMetals.com

www.TornadoBullion.com

X: @GrantOnGold

X: @ZanerMetals

Facebook: @ZanerPreciousMetals

Non-Reliance and Risk Disclosure: The opinions expressed here are for general information purposes only and should not be construed as trade recommendations, nor a solicitation of an offer to buy or sell any precious metals product. The material presented is based on information that we consider reliable, but we do not represent that it is accurate, complete, and/or up-to-date, and it should not be relied on as such. Opinions expressed are current as of the time of posting and only represent the views of the author and not those of Zaner Metals LLC unless otherwise expressly noted.