Zaner Daily Precious Metals Commentary

Friday, September 13, 20249/13/2024

Gold extends to more record highs as silver trades with a 30-handle for the first time in 8-weeks

OUTSIDE MARKET DEVELOPMENTS: North Korea released photos of Kim Jong Un touring a secret uranium enrichment facility. Kim said that Pyongyang needs to "exponentially increase" its nuclear weapons stockpile for "self-defense and the capability for a preemptive attack."

Just the mention of a potential nuclear first strike raises the risk factor in the region and globally. There is speculation that North Korea may be planning to run its first nuclear tests since 2017.

The timing of these provocative actions, just 52 days out from the U.S. presidential election, may be designed to send a message to the next U.S. administration. That message seems to be that the DPRK remains a destabilizing force in Asia and a foreign policy challenge for America.

On Thursday, a Wall Street Journal article by the influential Nick Timiraos suggested that a larger 50 bps Fed rate cut was not off the table. The probability of such a cut had tumbled into the teens after Thursday's inflation data but began climbing later in the session, ending at 28%. This morning the probability is at 43%.

Timiraos acknowledged that the Fed preferred to move in 25 bps increments but some policymakers are reportedly "nervous" about keeping rates too high for too long amid signs of mounting growth risks. The market continues to price in 100 bps of cuts by year-end, suggesting at least one of the three remaining FOMC meetings this year will have to end with a 50 bps cut. I continue to believe it won't be the first one.

News that the interest payment on the $35.3 trillion national debt cracked the $1 trillion barrier for the first time may provide additional incentive for the Fed to bring rates down. The government has paid $1.049 trillion to service the debt so far this year, up 30% from the same period last year. This is clearly unsustainable.

U.S. trade prices for August came in weaker than expected providing further evidence that inflationary pressures are moderating. The export price index fell by 0.7%, while import prices dropped 0.3%.

Preliminary Michigan sentiment for September rose to 69.0, versus 67.9 in August. Sentiment continues to improve from July's 8-month low at 66.4. The 1-year inflation index continued to fall, reaching a 45-month low of 2.7%.

GOLD

OVERNIGHT CHANGE THROUGH 6:00 AM CDT: +$7.98 (+0.31%)

5-Day Change: +$72.83 (+2.92%)

YTD Range: $1,986.16 - $2,581.46

52-Week Range: $1,812.39 - $2,5781.46

Weighted Alpha: +35.39

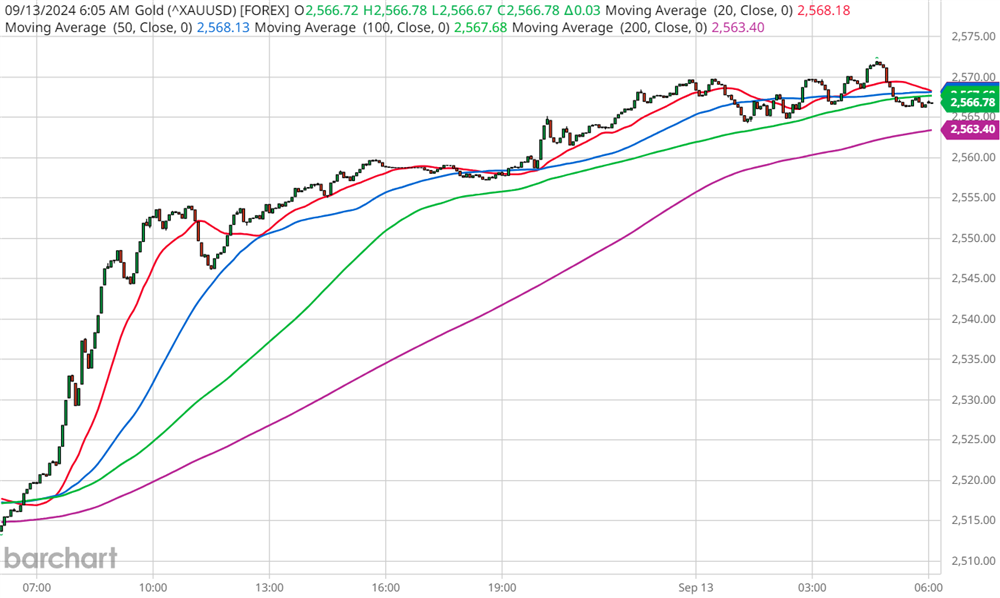

Gold continues its march higher on Friday after initially pushing to record levels in U.S. trading on Thursday. The yellow metal is up more than 3% this week and will post its first higher weekly close in three. Gold is up nearly 25% YTD.

The yellow metal is being buoyed by revived expectations that the Fed will launch its easing campaign next week, with a 50 bps cut. New lows for the week in the dollar index are providing an additional boost to gold today.

Given the magnitude of this week's rise and the developing overbought condition, there is potential to see some profit-taking ahead of the weekend. However, short-term setbacks are likely to be viewed as buying opportunities in anticipation of a test of $2,597.15/$2,600.00. Beyond that, the next Fibonacci level I'm watching is $2,619.35.

This week's gains have reignited talk about $3000 gold. I'm quoted in a recent Reuters article on that topic.

Besides falling interest rates, Joseph Cavatoni at the World Gold Council suggests uncertainty surrounding the upcoming U.S. election as another source of demand as investors seek to hedge event risk.

Intraday supports around $2,570.00 and at $2,564.67/26 protect the session low at $2,557.21.

SILVER

OVERNIGHT CHANGE THROUGH 6:00 AM CDT: +$0.121 (+0.41%)

5-Day Change: +$2.268 (+8.12%)

YTD Range: $21.945 - $32.379

52-Week Range: $20.704 - $32.379

Weighted Alpha: +32.52

Silver has surged to 8-week highs above $30.164, helped by record highs in gold and a weaker dollar. The white metal is up nearly 10% this week, the biggest weekly rise since mid-May.

The breach of a minor chart point mentioned in yesterday's comment at $30.584 (18-Jul high) lends credence to the scenario that calls for additional short-term gains to $31.00 and the July high at $31.652. While the May high at $32.379 looks increasingly attractive with each uptick, the volatility we've seen since that high was set warrants continued caution.

The previous highs at $30.164/082 mark first support. Secondary support is defined by the overseas low at $29.869.

Peter A. Grant

Vice President, Senior Metals Strategist

Zaner Metals LLC

Tornado Precious Metals Solutions by Zaner

312-549-9986 Direct/Text

[email protected]

www.ZanerPreciousMetals.com

www.TornadoBullion.com

X: @GrantOnGold

X: @ZanerMetals

Facebook: @ZanerPreciousMetals

Non-Reliance and Risk Disclosure: The opinions expressed here are for general information purposes only and should not be construed as trade recommendations, nor a solicitation of an offer to buy or sell any precious metals product. The material presented is based on information that we consider reliable, but we do not represent that it is accurate, complete, and/or up-to-date, and it should not be relied on as such. Opinions expressed are current as of the time of posting and only represent the views of the author and not those of Zaner Metals LLC unless otherwise expressly noted.