Zaner Daily Precious Metals Commentary

Monday, March 31, 2025Gold on track for biggest quarterly gain in almost 40 years

OUTSIDE MARKET DEVELOPMENTS: With new reciprocal tariffs set to take effect this week, risk-off sentiment continues to drive investors toward safe-haven assets. The S&P 500 is poised for its first losing quarter since Q3'23 and its biggest loss since Q3'22 amid heightened growth and price risks.

“We continue to believe the risk from April 2 tariffs is greater than many market participants have previously assumed,” said Goldman Sachs in a weekend note. Reports last week that President Trump had an “extremely productive call” with Canadian PM Carney, and rumblings of EU concessions have done little to temper trade war worries.

Goldman Sachs now sees three 25-bps rate cuts this year, beginning in July. The implied Fed funds rate for year-end is 3.5925% today, with 78.25 bps in easing priced in.

The Fed will likely focus on boosting growth because of the implications for employment. The argument is that weakening growth will reduce inflationary pressures. However, there are mounting concerns about stagflation.

Optimism about a ceasefire between Russia and Ukraine and movement toward a peace deal has dimmed. President Trump has expressed displeasure with both Vladimir Putin and Volodymyr Zelensky.

"If Russia and I are unable to make a deal on stopping the bloodshed in Ukraine, and if I think it was Russia's fault - which it might not be... I am going to put secondary tariffs... on all oil coming out of Russia," said Trump.

Israel has ordered that most of the southern Gaza city of Rafah be evacuated. This suggests Israel is preparing new ground operations.

Market focus this week will be on Friday's jobs report. The market is expecting a payrolls increase of 120k and an uptick in the jobless rate to 4.2%.

Chicago PMI rose 2.1 points to a 16-month high of 47.6 in March, above expectations of 45.4, versus 45.5 in February. It was the third straight monthly gain.

Dallas Fed Index tumbled 8 points to an eight-month low of -16.3 in March, versus -8.3 in February. The outlook uncertainty index pushed up seven points to 36.2, its highest reading since fall 2022, according to the Dallas Fed.

GOLD

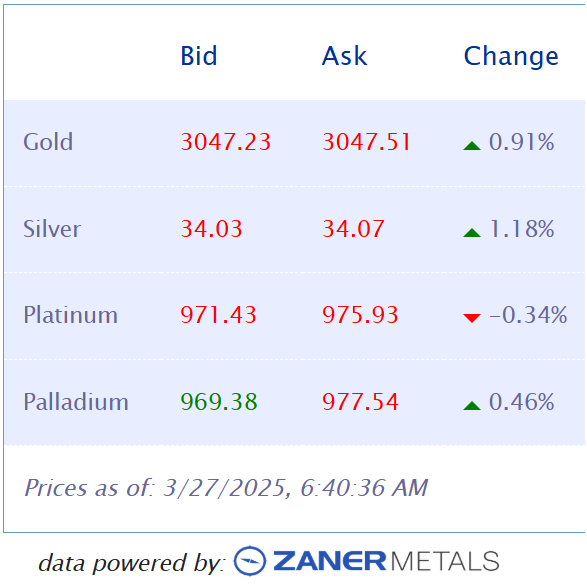

OVERNIGHT CHANGE THROUGH 6:00 AM CST: +$32.10 (+1.06%)

5-Day Change: +$110.80 (+3.68%)

YTD Range: $2,607.16 - $3,123.98

52-Week Range: $2,231.10 - $3,123.98

Weighted Alpha: +38.19

Gold extended to the upside on the last trading day of March and Q1, reaching a new all-time high of $3,124.93. The yellow metal is up 9% this month and is poised for its best quarterly performance since 1986.

The rally continues to be driven by tariff worries, elevated inflation expectations, a soft dollar, and persistent central bank demand. Today's push above $3,100 bodes well for attainment of the $3,149.84 Fibonacci objective and lends additional credence to the longer-term target at $3,500.

Morgan Stanley strategist Amy Gower sees gold topping out at $3,300/$3,400 this year as record-high prices sap all-important jewelry demand. However, Goldman Sachs suggested gold could reach $4,500 over the next 12 months in an "extreme tail scenario.”

While the WGC hasn't updated ETF data for last week, I suspect a ninth straight weekly inflow into gold ETFs will be confirmed.

The COT report for last week showed that net speculative long positions held steady at 257.9k contracts.

A minor intraday chart point at $3,105.29 marks first support and protects the $3,100.00 level. More important support is defined by today's Asian low at $3,078.93. The 20-day moving average is poised to climb above $3,000 this week.

OVERNIGHT CHANGE THROUGH 6:00 AM CST: -$0.056 (-0.16%)

5-Day Change: +$1.128 (+3.42%)

YTD Range: $28.946 - $34.543

52-Week Range: $24.801 - $34.853

Weighted Alpha: +25.53

Silver is trading lower for a second straight session, but is still nearly 9% higher for March and more than 17% for Q1. While the latest record highs in gold and a soft dollar are seen as supportive, mounting trade war concerns and global growth risks have weighed more recently.

The same worries have knocked copper off its recent record highs, providing an additional headwind for silver. Copper prices in the U.S. were up 28% YTD last week, as manufacturers loaded up on the important metal ahead of threatened tariffs. The Wall Street Journal declared, Copper Is 2025’s Hottest Commodity.

While silver scored five-month highs last week, gains stalled ahead of the key $34.853 peak from October. A breach of this level is needed to perpetuate the uptrend and shift focus to the $35.348 high from October 2012.

I suspect the trade will want to try a more serious challenge of that October peak, so downticks are considered corrective at this point. Last week's high at $34.543 is an important intervening barrier.

The COT report for last week showed net speculative long positions held steady at 62.3k contracts.

CFTC Silver speculative net positions

Minor chart support marked by Thursday's low at $33.618 has contained the downside today. This keeps Wednesday's low at $33.521 and the more important 20-day moving average at $33.342 at bay.

Peter A. Grant

Vice President, Senior Metals Strategist

Zaner Metals LLC

312-549-9986 Direct/Text

[email protected]

www.zanermetals.com

Non-Reliance and Risk Disclosure: The opinions expressed here are for general information purposes only and should not be construed as trade recommendations, nor a solicitation of an offer to buy or sell any precious metals product. The material presented is based on information that we consider reliable, but we do not represent that it is accurate, complete, and/or up-to-date, and it should not be relied on as such. Opinions expressed are current as of the time of posting and only represent the views of the author and not those of Zaner Metals LLC unless otherwise expressly noted.