3/26/2025

Gold and silver consolidate recent gains, but uptrends remain highlighted

OUTSIDE MARKET DEVELOPMENTS: The Trump administration's ever-changing positions on tariffs and trade continue to stoke market uncertainty. Concerns that these policies will weigh on economic growth and revive inflation have heightened risk aversion and contributed to market volatility.

Consumption is the major driving force behind the U.S. economy, and high levels of uncertainty have eroded consumer sentiment in recent months. The Conference Board Consumer Confidence Index tumbled 7.2 points in March to a four-year low of 92.9.

"Consumers’ expectations were especially gloomy, with pessimism about future business conditions deepening and confidence about future employment prospects falling to a 12-year low," said Stephanie Guichard, Senior Economist, Global Indicators at The Conference Board.

The Atlanta Fed's GDPNow forecast for Q1 remained in negative territory at -1.8% for the 18-Mar reading, and the blue chip consensus has fallen below +2.0%. An update is slated for today.

The NY Fed's NowCast continues to paint a rosier picture, with a 2.72% Q1 estimate on 21-Mar.

Prospects for a June Fed rate cut have risen lately. The implied Fed funds rate for December is currently 3.7475%, reflecting expectations for 63 bps in easing by year-end.

Minneapolis Fed President Kashkari believes there is more work to be done on inflation, but sees policy uncertainties complicating the Fed's job. Nonetheless, he still thinks the central bank "ought to be able to reduce interest rates further" in the next year or two.

Russia and Ukraine have reportedly agreed to a ceasefire in the Black Sea. "All parties have agreed to ensure safe navigation, eliminate the use of force, and prevent the use of commercial vessels for military purposes in the Black Sea," said Ukrainian Defense Minister Rustem Umerov.

A broader ceasefire and peace deal remain elusive. However, this limited agreement is arguably progress and dials down the temperature in the region somewhat.

MBA Mortgage Applications fell 2.0% in the 21-Mar week, versus -6.2% in the previous week. The 30-year mortgage rate ticked down to 6.71%.

Durable Orders unexpectedly rose 0.9% in February, well above expectations of -1.2%, versus a revised +3.3% in January (was +3.1%). Ex-trans rose 0.7%, and shipments were +1.2%.

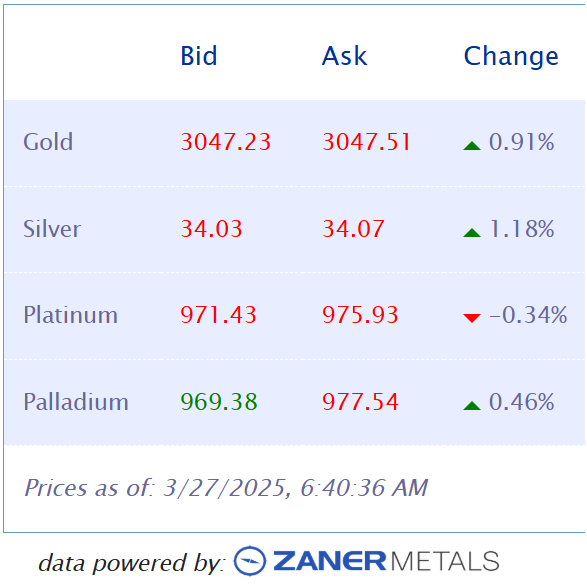

GOLD

OVERNIGHT CHANGE THROUGH 6:00 AM CST: +$3.55 (+0.12%)

5-Day Change: -$21.19 (-0.70%)

YTD Range: $2,607.16 - $3,056.51

52-Week Range: $2,174.69 - $3,056.51

Weighted Alpha: +36.79

Gold is consolidating above $3,000 and within striking distance of last week's record high of $3,056.51. The yellow metal continues to be underpinned by haven interest stemming from tariff uncertainty and geopolitical risks.

Four sessions of corrective/consolidative price action have somewhat relieved the overbought condition that developed last week. While further tests of the downside can not be ruled out, the trade should continue to view setbacks as buying opportunities.

The market is certainly good as long as it's above $3,000. A minor secondary chart point is noted at $2,982.85/$2,980.54. More important support is marked by the previous high at $2,955.40, which is now bolstered by the 20-day moving average at $2,960.12.

A short-term breach of last week's high at $3,056.51 would lend additional credence to the bullish scenario that calls for a push to $3,100. Beyond that, the next Fibonacci objective at $3,149.84 attracts.

BofA has upgraded its 2025 gold forecast to $3,063 from $2,750 previously. They now see gold at $3,350 in 2026, a $725 increase over their previous forecast of $2,625!

The bank believes the yellow metal could climb to $3,500 in the next two years if investment demand increases by 10%. They also think central banks could increase gold reserves from current levels around 10% to 30%! That would provide a huge tailwind for gold that could take prices beyond $4,000 in my opinion.

Recent ETF inflows suggest investors do indeed have increased interest in gold. Global ETF inflows were 31.3 tonnes last week, with North American investors accounting for nearly all of that. It was the eighth consecutive weekly inflow.

ETF.com data revealed that flows into the GLD ETF reached $2 billion on Monday. "This rush into gold signals a broader shift in sentiment—investors are diversifying away from U.S. assets, concerned about rising geopolitical risks, trade tensions and central bank policies that may further weaken the dollar," wrote CFP Kent Thune on ETF.com.

"As gold strengthens, a self-reinforcing cycle has emerged: A weaker U.S. dollar makes gold more attractive to global investors, driving up demand, which in turn pushes prices higher and further erodes confidence in the dollar," added Thune.

SILVER

OVERNIGHT CHANGE THROUGH 6:00 AM CST: +$0.036 (+0.11%)

5-Day Change: +$0.063 (+0.19%)

YTD Range: $28.946 - $34.208

52-Week Range: $24.344 - $34.853

Weighted Alpha: +33.17

Silver set a new high for the week at $33.897 in early U.S. trading before retreating into the range. The white metal continues to be underpinned by Chinese stimulus and German spending expectations.

Soaring copper prices are providing additional lift to silver. The two markets are pretty tightly correlated, as silver is primarily a byproduct of copper mining.

Copper has reached record highs on worries about shortages and front-running ahead of impending tariffs. Additionally, Glencore declared force majeure on shipments from its Altonorte smelter in Chile due to a furnace issue.

A climb back above $34 would bode well for the continuation of the uptrend off the December lows. A breach of last week's high at $34.208 would bode well for the expected retest of the more than 22-year high set in October at $34.853. Beyond the latter, the $35.348 high from October 2012 would be in play.

Today's overseas low at $33.570 marks first support. More substantial supports at $32.904 (Monday's low) and $32.767 (Friday's low) appear well protected at this point. The 20-day MA is at $32.930 and bolsters the secondary support zone.

Peter A. Grant

Vice President, Senior Metals Strategist

Zaner Metals LLC

312-549-9986 Direct/Text

[email protected]

www.zanermetals.com

Non-Reliance and Risk Disclosure: The opinions expressed here are for general information purposes only and should not be construed as trade recommendations, nor a solicitation of an offer to buy or sell any precious metals product. The material presented is based on information that we consider reliable, but we do not represent that it is accurate, complete, and/or up-to-date, and it should not be relied on as such. Opinions expressed are current as of the time of posting and only represent the views of the author and not those of Zaner Metals LLC unless otherwise expressly noted.