Grant on Gold – October 16, 2023

Monday, October 16, 2023Gold surged nearly 5.5% last week, spurred by safe-haven buying in the wake of the horrific October 7th attack on Israel. While downside retracement was seen on Monday, the initial push back above the $1900 level leaves the low end of the bear channel well protected for the time being.

With an Israeli ground offensive into Gaza thought to be imminent, and amid worries that the conflict could expand, look for the yellow metal to remain underpinned. Iran has warned Israel of “far reaching consequences” should they launch a ground invasion.

Gold is garnering additional lift from rising hopes that the Fed is done raising rates this year. The CME’s FedWatch tool puts the probability of a November rate hike at just 5.2%, while the odds for a December rate hike stand at 32.7%.

While PPI rebounded in September to 2.2% y/y, and CPI held steady at 3.7%, members of the Fed still seem to be encouraged by the progress in the fight against inflation.

“Absent a stark turn in what I see in the data and hear from contacts … I believe that we are at the point where we can hold rates where they are,” said Philadelphia Fed President Patrick Harker. Raphael Bostic of the Atlanta Fed stated last week that he does not believe that the FOMC needs to hike again.

There is still a wide belief that the Fed’s next move is very data-dependent. The present stance has been categorized as a “hawkish hold.” As long as the trajectory for inflation is down, the central bank will likely keep rates as they are.

Monday’s low at $1908.23 now provides a good intervening support level ahead of the 38.2% retracement level of the rally off the $1810.46 low, which comes in at $1886.14.

On the upside, the next tier of resistance is found at $1947.46/$1953.06. A breach of this area would exceed the halfway back point of the entire decline off the $2067.00 high from May, shifting focus to the 61.8% retracement level at $1969.00.

As long as geopolitical tensions remain elevated and nearby supports are intact, setbacks into the range are likely to be viewed as buying opportunities.

While haven flows have gold and the dollar moving generally in tandem at the moment, keep an eye on that relationship for short-term directional cues.

Silver

Silver rose just over 5% last week as outside forces stoked market volatility. Despite the strong rally, additional gains are needed to set a more favorable technical tone.

A rebound above $23.41 would constitute a 50% retracement of the decline from the May high at $26.14. It would also put silver back above its 100- and 200-day moving averages. This would have rather bullish implications.

A retreat below $21.80/75 would return focus to the bearish scenario that has dominated since the downside breakout of the large triangle pattern. Such a move would return focus to the $20.68 low from October 3 and highlight the low for the year at $19.90 once again.

While silver followed gold higher last week, the white metal is probably more concerned about the implications of another war on regional and global growth, as well as prices. If signs of stagflation begin to surface, silver would likely remain defensive.

PGMs

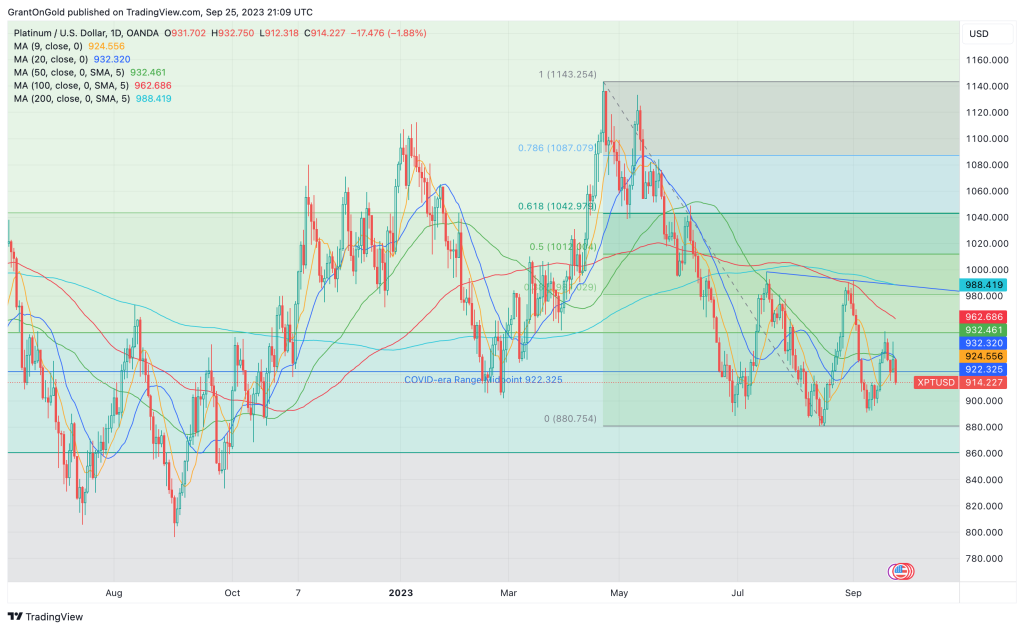

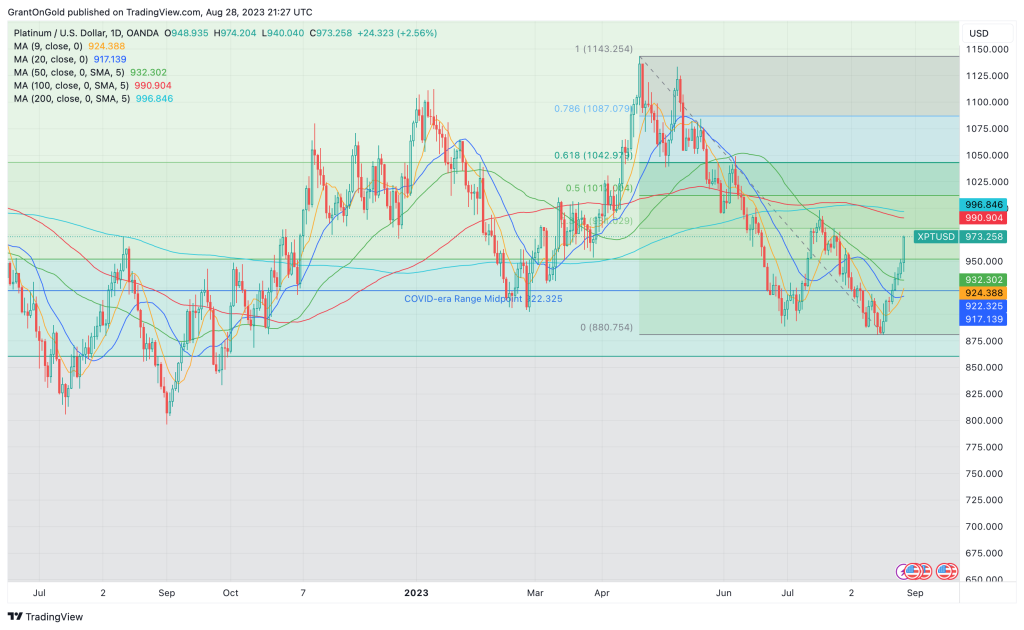

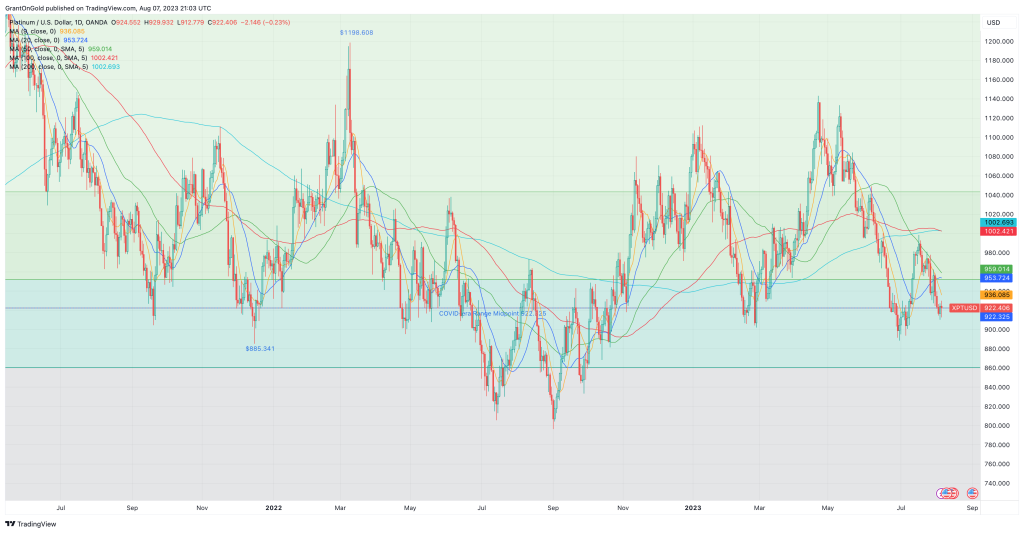

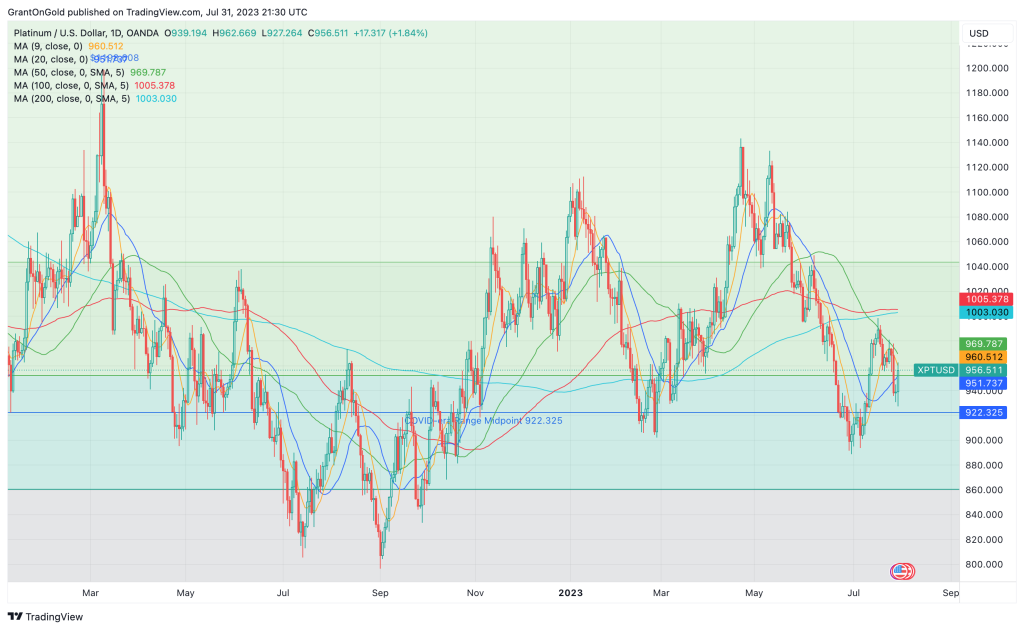

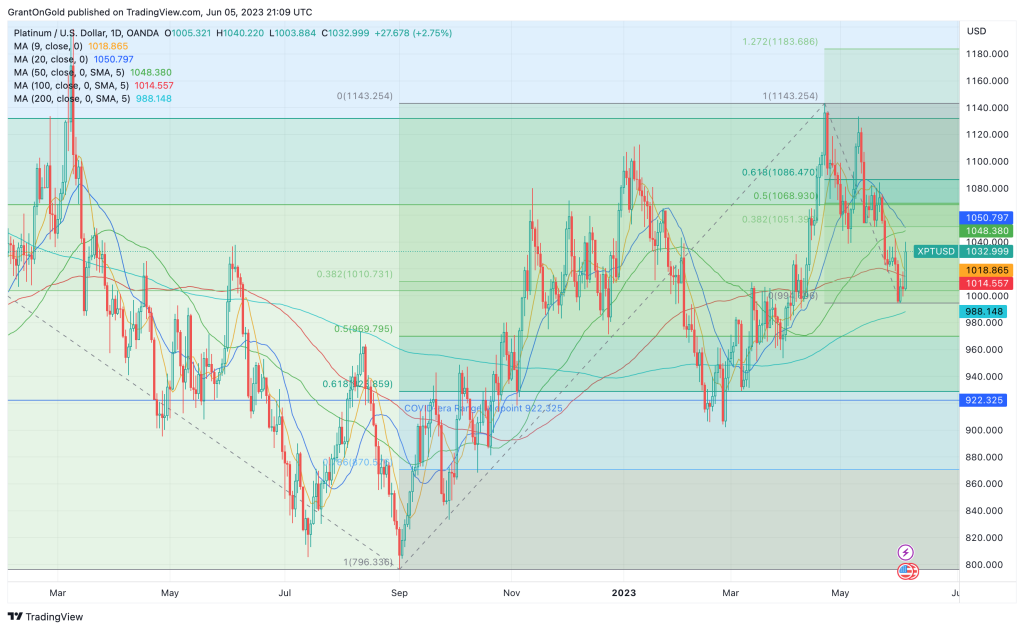

Platinum was comparatively subdued last week, rising a scant 0.5% with activity confined to the previous week’s range. Consolidative trading prevailed on Monday.

The short-term technical bias remains negative with platinum below the midpoint of the COVID-era range and all the important moving averages.

Palladium remains weak after sliding to fresh 5-year lows two weeks ago. The next support level to watch is defined by a measuring objective and a Fibonacci level at $1088.38/$1085.50.

Non-Reliance and Risk Disclosure: The opinions expressed here are for general information purposes only and should not be construed as trade recommendations, nor a solicitation of an offer to buy or sell any precious metals product. The material presented is based on information that we consider reliable, but we do not represent that it is accurate, complete, and/or up-to-date, and it should not be relied on as such. Opinions expressed are current as of the time of posting and only represent the views of the author and not those of Zaner Metals LLC unless otherwise expressly noted.

.png)