With the dollar posting another higher high for the move and approaching the 106.00 level, currency pressure on gold and silver continues to increase.

However, yesterday gold and silver showed they could avoid wholesale liquidations, but further pressure today could result in a fresh wave of stop-loss selling.

While the higher for longer interest rate mantra remains on the back of most markets the markets will be presented with a series of US housing price and sales readings today which have been showing signs of softening that could temporarily undermine the dollar...[MORE]

Please subscribe to receive the full report via email by clicking here.

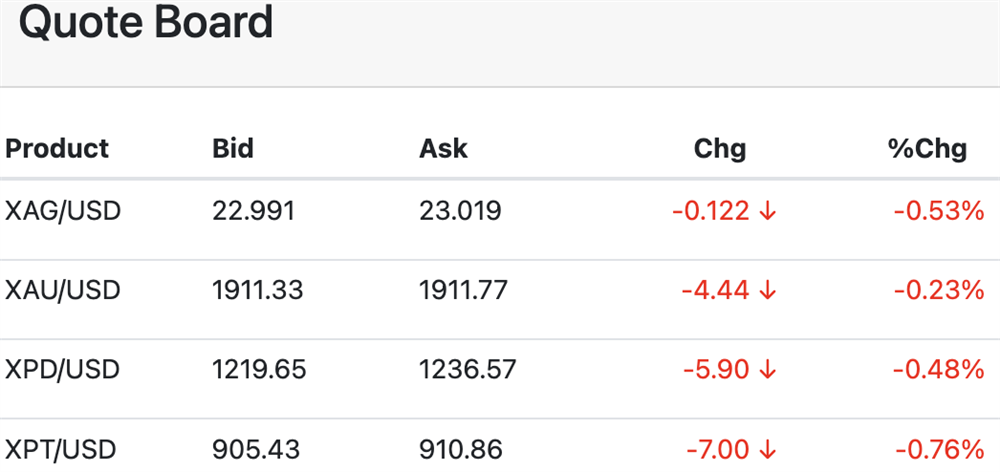

Sep 26 (Reuters) - Gold prices fell on Tuesday, as bullion’s appeal dimmed in the face of a stronger U.S. dollar and higher Treasury yields, while investors strapped in for key inflation data this week for further rate guidance on U.S. rates.

Spot gold edged down 0.2% to $1,912.79 per ounce by 0952 GMT, its lowest since Sept. 15, while U.S. gold futures fell 0.3% to $1,931.50...[LINK]

Good morning. The precious metals are lower in early U.S. trading.

U.S. calendar features Case-Shiller Home Price Index, FHFA Home Price Index, Consumer Confidence, New Home Sales, Richmond Fed Index, M2, #FedSpeak from Bowman.

Gold continues to consolidate in the bearish channel that dominated throughout the summer. The 100-day MA successfully contained the upside last week, leaving the downside vulnerable to further tests.

Spot Gold Daily Chart through 9/25/2023

Last week the Fed held steady on rates, as was widely expected. However, Chairman Powell noted strength in the economy and his desire to see “convincing evidence” that inflation is moderating.

The dot plot suggested that at least one more rate hike could be seen this year. Perhaps more importantly, the dots reinforced the ‘higher for longer’ scenario with the first rate cut now forecast for June 2024.

The 10-year yield moved more convincingly above 4% on Monday, reaching levels not seen since 2007. Higher yields are buoying the greenback. The dollar index extended on Monday to reach 10-month highs.

Higher yields and a higher dollar will continue to pose a considerable headwind for gold. Mounting global growth risks apply additional weight.

It is believed that the Eurozone economy contracted in Q3, even as inflation remains elevated. September CPI is forecast to be 4.5%. While that’s down from 5.2% in August, the inflation rate remains well above target.

Earlier in the month, the ECB hiked rates for a 10th consecutive meeting, pushing the deposit rate to a record high of 4%. Analysts now believe the ECB is on hold, probably into next summer.

However, the ECB also will want to see some convincing evidence to confirm that inflation has been squelched in the EU. Until that happens, at least one more rate hike can’t be ruled out.

Of course, worries about the Chinese economy persist as well. This could have grim implications for the global economy.

Chinese demand for imports has contracted in nine of the last 10 months. If China slips into recession, there are concerns that demand for commodities will suffer further. While that may help tamp inflation, the demand destruction will be the greater concern in the medium term.

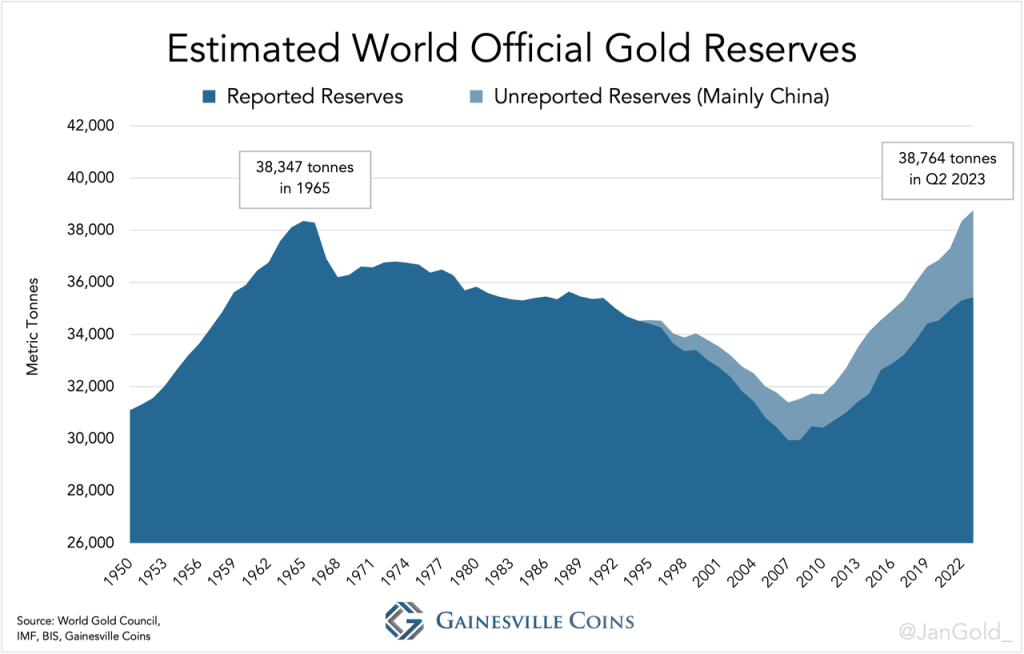

The ongoing expansion of official gold reserves remains a bright spot for the yellow metal. Central banks continue to seek diversification, mainly out of dollars and into gold.

While central bank gold demand slowed in Q2, the record purchases in Q1 led to record H1 demand of 387 tonnes. Turkey was a big seller in April and May before resuming purchases in June.

The World Gold Council believes the Turkish sales were “tactical rather than strategic” amid internal economic and political strife. Interestingly, as the TCMB was selling, demand for bars, coins, and gold jewelry surged in the country as citizens sought to protect their wealth against a devaluing lira.

Estimated World Official Gold Reserves

Taking into consideration estimates of China’s unreported gold reserves, analyst Jan Nieuwenhuijs of Gainesville Coins believes world reserves reached an all-time high of 38,764 tonnes in Q2. If that’s an accurate assessment, it exceeds the previous record of 39,347 tonnes from 1965.

Nieuwenhuijs points out that gold as a percentage of total global reserves currently stands at 17%, while the long-term historical average is 58%. That suggests there remains considerable potential for further central bank gold buying.

If gold were once again to make up the majority of global reserves, one of Jan’s models projects a price in excess of $8,000 over the next 10 years.

Silver

Silver continues to trade in a choppy manner within the confines of a large symmetrical triangle pattern. The white metal rose more than 2% last week, but most of those gains were given back on Monday.

Spot Silver Daily Chart through 9/25/2023

The silver market is facing some of the same headwinds as the gold market. Perhaps most notably, sluggish demand for electronics in China is likely to adversely impact demand for silver.

The Chinese auto sector returned to growth in August, after contracting in June and July. Sales surged 8.5% m/m and 2.2% y/y with electric vehicles such as Teslas increasingly popular. However, the sustainability of these gains is in doubt as China’s real estate crisis threatens to sap consumer demand.

Real estate is the biggest contributor to Chinese GDP, so the crisis has the potential to drag the middle kingdom into recession. Growth risks in the world’s second-largest economy pose considerable risks to the global economy as a whole.

That being said, the global trend toward electrification keeps the long-term supply/demand fundamentals undeniably positive. Therefore, retreats into the range that has emerged this year are still likely to be viewed as buying opportunities.

Initial support is well-defined by the series of lows at $22.30, $22.22, and $22.11. This zone should keep the low for the year at $19.90 (10-Mar) at bay.

Last week’s high at $23.78 is now seen as the trigger for a retest of the upper reaches of the triangle pattern, which comes in around $24.50.

PGMs

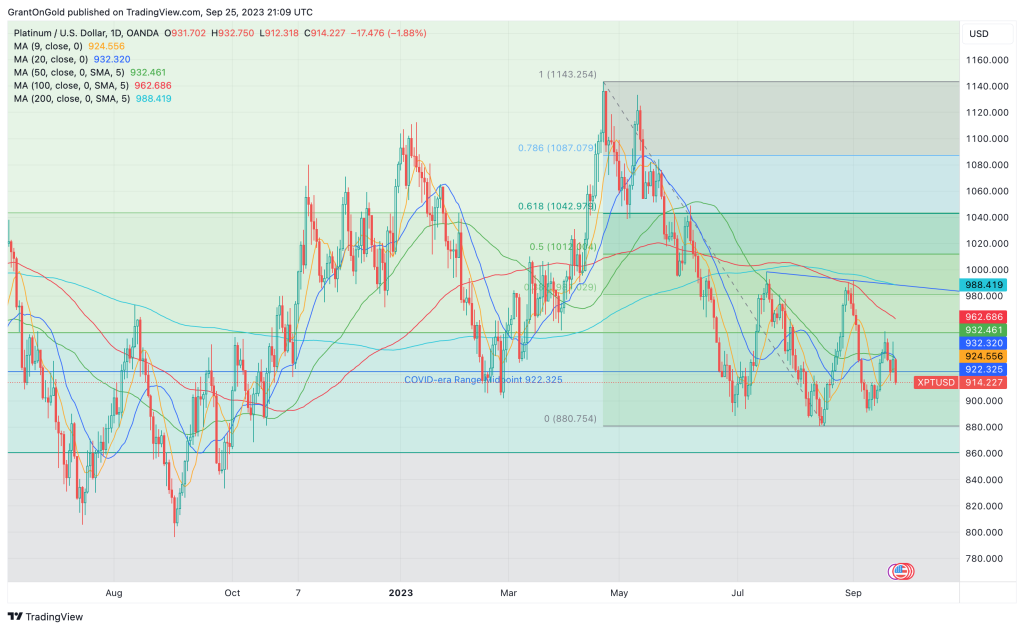

Platinum continues to struggle on upticks. The market rose modestly last week, notching a second consecutive higher weekly close. However, renewed selling pressure surfaced on Monday.

Spot Platinum Daily Chart through 9/25/2023

While U.S. auto sales were robust in August, global growth concerns continue to percolate below the surface. Rising interest rates also threaten to undermine consumer purchasing power.

Late-summer sales were helped by better supply, but if the expanding UAW strike persists the supply of new cars will tighten.

Palladium remains defensive at the low end of the multi-year range.

Non-Reliance and Risk Disclosure: The opinions expressed here are for general information purposes only and should not be construed as trade recommendations, nor a solicitation of an offer to buy or sell any precious metals product. The material presented is based on information that we consider reliable, but we do not represent that it is accurate, complete, and/or up-to-date, and it should not be relied on as such. Opinions expressed are current as of the time of posting and only represent the views of the author and not those of Zaner Metals LLC unless otherwise expressly noted.

Fortunately for gold and silver, bearish influences from the dollar and treasuries abated at the end of last week. Still, unfortunately, adverse trend action in those markets has returned and is likely to keep gold and silver under liquidation watch.

In fact, this morning global markets were rife with concerns that interest rates were set to remain high for longer firming the dollar and undermining most physical commodities.

Therefore, further gold price retrenchment from treasury and dollar market action likely push December gold down to the September lows of $1,921 and potentially press silver back to first support of $23.36 in the December contract...[MORE]

Please subscribe to receive the full report via email by clicking here.

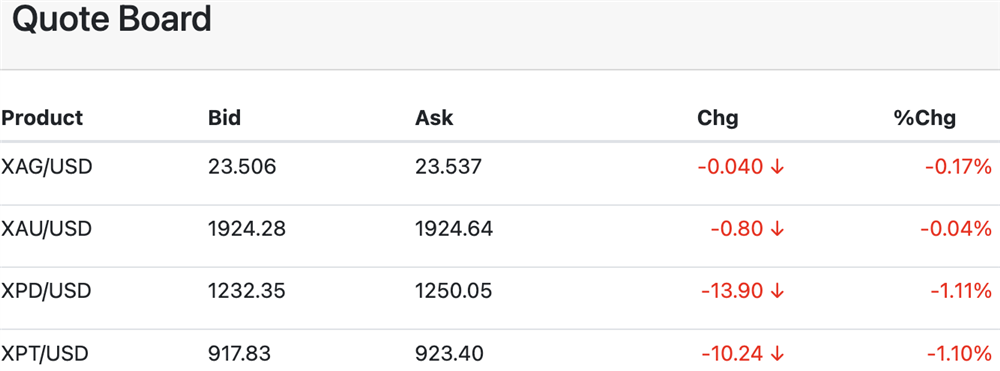

Sep 25 (Reuters) - Gold eased on Monday as the U.S. dollar stood strong after U.S. Federal Reserve officials flagged that interest rates would remain higher for longer, although moves were limited as investors look forward to inflation data later this week.

Spot gold was down 0.1% to $1,923.94 per ounce by 1153 GMT, while U.S. gold futures also fell 0.1% to $1,943.70...[LINK]

With the dollar bulls surviving and then thriving in the wake of a pause by the US #Fed and a downside breakout in US initial claims yesterday the uptrend in the dollar looks to expand.

Furthermore, given the bearish addition of a significant leap in US interest rates the path of least resistance in gold remains down.

However, the divergence between gold and silver makes us suspicious of the rally in silver which could result in a short sale opportunity if December silver reaches $24.25...[MORE]

Please subscribe to receive the full report via email by clicking here.

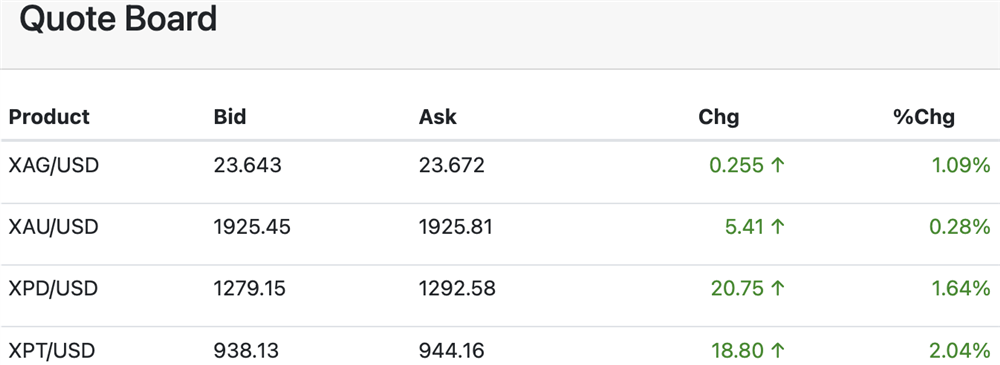

Sep 22 (Reuters) - Gold prices edged higher on Friday following weak economic data out of Europe and a week of key central banks deciding to stand pat on interest rates, although a stronger dollar kept bullion gains in check.

Spot gold was up 0.3% at $1,925.50 per ounce, as of 1152 GMT, following three sessions of losses. U.S. gold futures rose 0.4% to $1,946.20...[LINK]